February 2020 was one of the most active months on record for home purchases and refinances. According to the National Association of Realtors, sales of single-family homes, condos, and co-ops were the highest they've been in 13 years. More than 60% of all applications were for home refinances. By early March, however, the coronavirus outbreak had started to limit most in-person transactions. With mortgage rates at their lowest in nearly 50 years, how can someone purchase a house during this time of social distancing?

There are several questions to consider before buying a home during this time:

- How stable is your job? Will social distancing over a prolonged period negatively impact the profitability of the company you work for?

- How much of a down payment can you afford? If you need to use part of your savings to make a down payment, will you still have enough to cover future emergencies?

- Is it necessary for you to move now, or can you wait a few months? According to a Mortgage Report survey, rates are expected to stay low throughout 2020, so if you can wait, you may want to ride out the virus.

While buyers should proceed cautiously, there are several benefits to purchasing a home right now.

Less Competition From Home Buyers

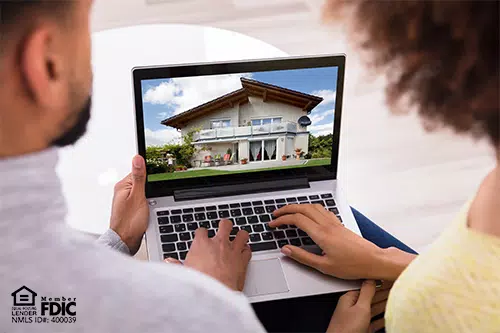

One of the main advantages of purchasing a home right now is that there's less competition. A lack of inventory had been one of the biggest obstacles for home buyers before the COVID-19 outbreak, but now that more buyers will be holding off, there's a better chance of getting your offer accepted. Conversely, some sellers are taking their homes off the market because they don't want to host open houses. So, without an open house or a realtor willing or able to show a home, how can you get a glimpse of a prospective new place to live?

Terry Jackson, a realtor at Domicile One Realty in Kansas City, says the safety of the client is the most important thing. "Our top priority is the safety of our clients and the community. We comply with stay-at-home orders by interacting with our clients using pre-recorded video showings, virtual tours, electronic signatures for contract documents, and video conferencing for meetings. Methods such as these are no longer a simple convenience. They are now absolutely vital to our ability to serve our clients," says Jackson.

Eased Home Appraisal, Inspection Requirements

This month, the Federal Housing Finance Agency announced that it is directing Fannie Mae and Freddie Mac to relax their standards for both property appraisals and employment verification. The FHFA states that "to allow for homes to be bought, sold, and refinanced as our nation deals with the challenges of the coronavirus, (Fannie Mae and Freddie Mac) will leverage appraisal alternatives to reduce the need for appraisers to inspect the interior of a home for eligible mortgages." This exterior inspection flexibility, however, does not apply to cash-out refinances, and there are restrictions on rate and term refinances.

Additionally, the FHFA will allow lenders to obtain employment verification confirmation via email from the employer if they are unable to obtain verbal verification.

The Federal Housing Administration (FHA) and the Department of Veterans Affairs followed suit quickly. They made similar changes to allow appraisal and income verification alternatives for their FHA loans and VA loans. The FHA and VA will now allow exterior-only appraisals, also known as drive-by appraisals, and, in some instances, desktop appraisals. In these cases, the appraiser relies on public records, multiple listing service information, and other third-party sources.

For income verification, the FHA will now allow year-to-date pay stub or direct electronic verification of income dated immediately before note date or bank statements showing a direct deposit from the borrower's employer for the pay period immediately before the settlement date. The VA recommends lenders use "employment and income verification third-party services" or verify through "evidence of direct deposit from a bank statement and pay stubs covering at least one full month of employment within 30 days of the closing date."

Securing the Home Loan

Most mortgage lenders can process your loan over the phone. Joseph Watts, senior vice president of Residential Lending at North American Savings Bank, says the COVID-19 outbreak has not hampered their ability to help clients get loans:

"We still provide the level of service to our customers they have come to expect. Some delays are inevitable with historically low rates, consumer demand, and stay at home orders across the country. Yet, with all these challenges, the staff is committed to providing outstanding service and closing loans as quickly as possible," says Watts.

If you still have questions about whether purchasing a home during the coronavirus outbreak is a good idea, contact your financial planner or lender to discuss your options.

At NASB we're ready to answer any questions about purchasing during this difficult time. Just give us a call at 888-661-1982.